STRATEGIC ANALYSIS

The Competitive Landscape of Nuclear Waste Management and Recycling

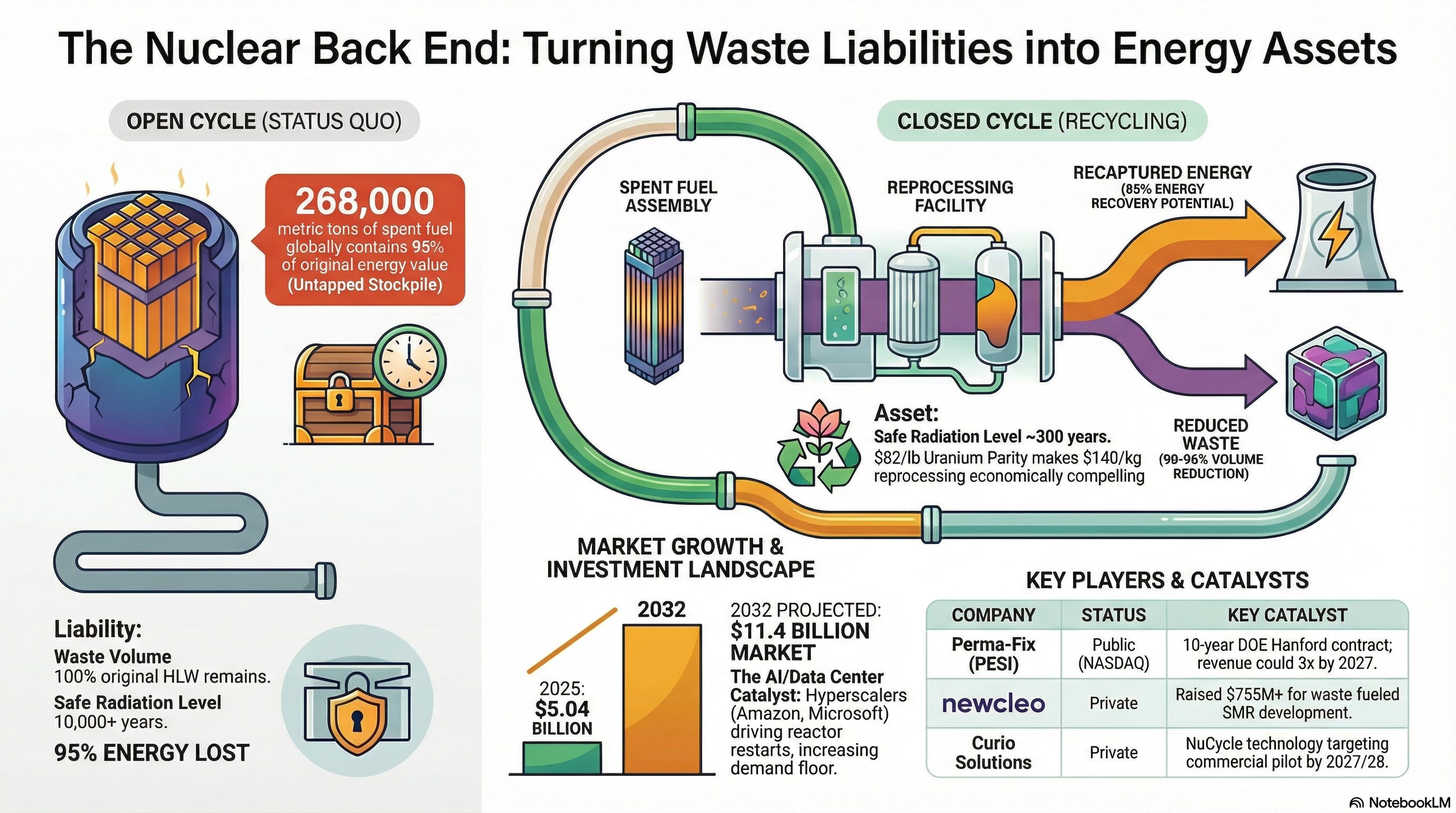

Strategic Taxonomy: Distinguishing the Open vs. Closed Fuel Cycle

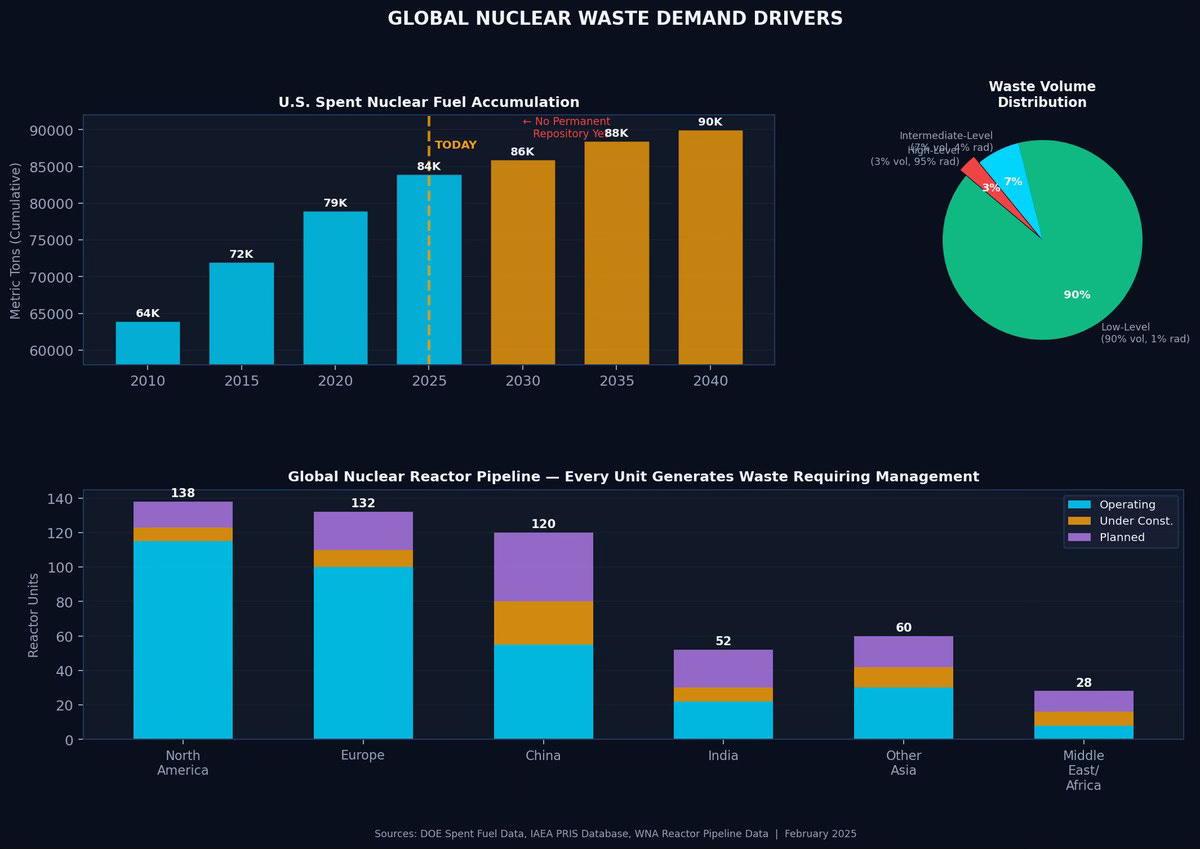

The nuclear industry is undergoing its most profound strategic pivot since the dawn of the atomic age: the transition from a “disposal-first” (Open Cycle) mindset to a “resource-recovery” (Closed Cycle) model. Historically, the back end of the fuel cycle was viewed as an expensive, politically radioactive liability—a cost center to be minimized. However, as AI-driven power demand and carbon-neutral mandates compress the global energy supply, the 268,000 metric tons of spent fuel globally are being re-evaluated as an untapped fuel stockpile containing 95% of its original energy value.

Think of this shift through the lens of Water Rights in the American West. For decades, the infrastructure and legal obligations surrounding nuclear waste were ignored while capital chased the “cattle and land” of reactor construction and uranium mining. Now, the market is realizing that the infrastructure controlling the waste also controls a permanent, multi-century resource.

With the total U.S. disposal liability estimated at over $96 billion, the economic incentive to transform this liability into an asset has reached a critical inflection point.