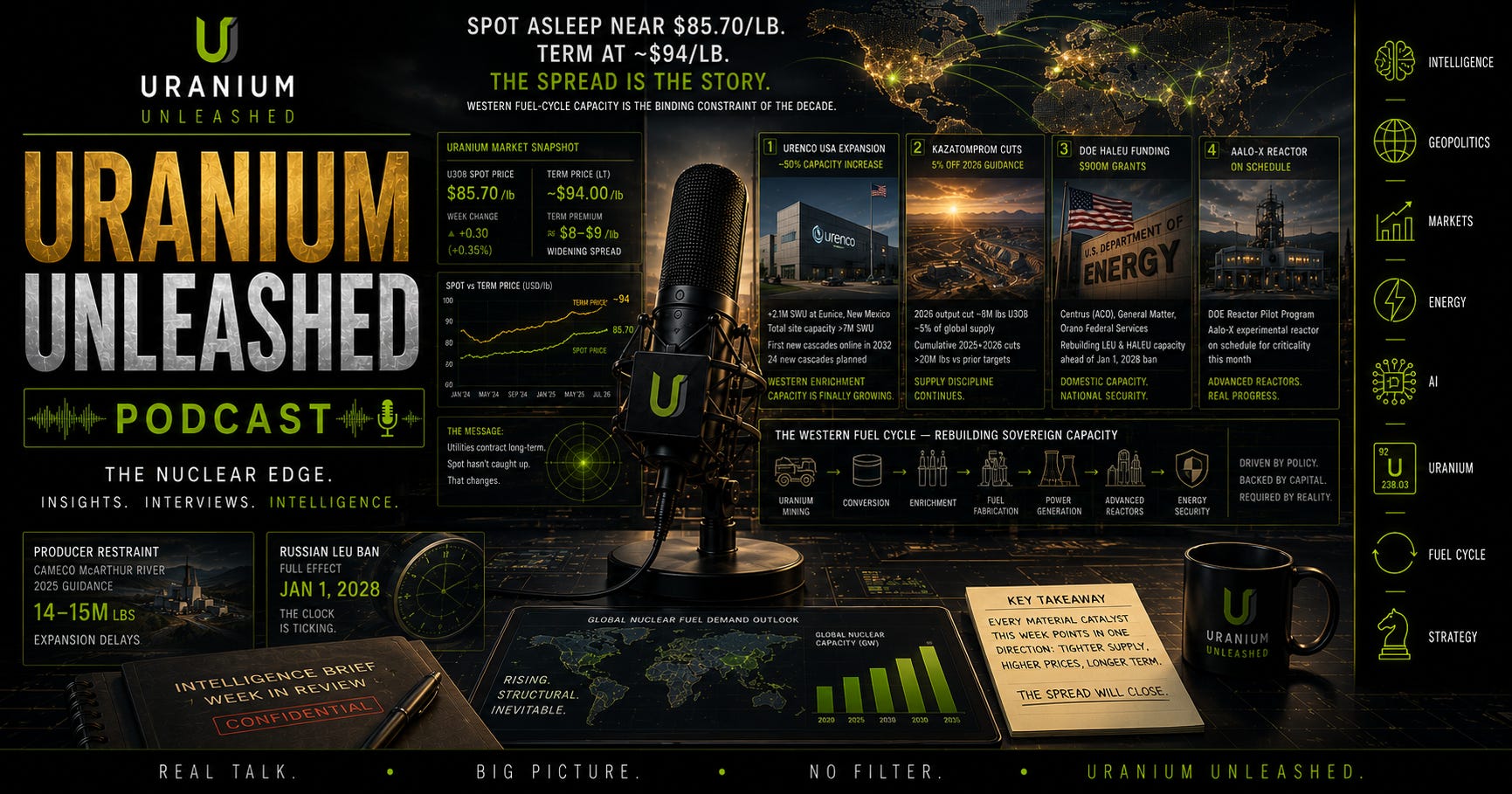

The growing chasm between uranium’s sleepy spot market and its surging long-term contract market reveals a Western fuel cycle bracing for a structural supply crisis. While spot prices quietly drifted within an $84 to $87 band to close the week near $85.70 per pound, long-term contract prices held firm at $94 per pound. This nearly $9 spread represents the widest sustained gap of the entire cycle, signaling that utility fuel buyers have entered a queue of forward demand as they actively prioritize long-term delivery security over immediate spot purchases. This episode of Uranium Unleashed: The Week in Review unpacks this dual-reality pricing model and explores how major physical catalysts are driving the nuclear fuel industry toward a major spot re-rating.

At the heart of the tightening Western fuel cycle is a massive commitment of real capital to domestic enrichment capacity, led by Urenco USA’s plan to expand its Eunice, New Mexico facility by nearly 50%. By adding up to 24 centrifuge cascades and 2.1 million SWU, Urenco plans to push the site’s total capacity past 7 million SWU. Though the first new cascades will not arrive until 2032, this timeline immediately forces utilities to reprice their enrichment risk ahead of the impending January 1, 2028 full ban on Russian low-enriched uranium (LEU) imports. This commercial buildout is heavily reinforced by policy, as demonstrated by the Department of Energy’s $900 million HALEU grants recently placed with Orano Federal Services, General Matter, and Centrus subsidiary American Centrifuge Operating to ensure a secure domestic fuel pipeline.

On the mining side of the ledger, persistent supply discipline from the world’s two largest producers continues to starve the term market of excess volume. Kazatomprom’s 5% cut to its 2026 production guidance has effectively removed 8 million pounds of U3O8 from the global supply curve, while Cameco’s McArthur River joint venture is guided at 14 to 15 million pounds for 2025 due to expansion delays. Combined, these actions have pulled over 20 million pounds of uranium relative to prior targets, cementing a structural regime shift where producers comfortably hold the pricing power. Rather than chase a quiet spot market, these mining majors are successfully dictating terms to utilities, which are being forced to sign long-term contracts at high premiums to secure future volumes.

The demand side is also flashing accelerated timelines, headlined by the Department of Energy’s Reactor Pilot Program as Aalo Atomics’ experimental Aalo-X reactor targets first criticality this month. If successful, this regulatory and political momentum will provide a clear pathway for advanced reactors that will eventually contract for long-term fuel. Looking ahead, the market will closely monitor this criticality window alongside preparing for Kazatomprom’s late-July operating update and Cameco’s upcoming Q2 earnings window to see if further supply contractions will finally spark a spot market catch-up.