THE STRATEGIC PAUSE Infrastructure Realignment in the AI–Nuclear Nexus

How Grid Bottlenecks, Equipment Shortages, and Political Headwinds Are Reshaping the Data Centre Boom — and What It Means for the Nuclear Sector

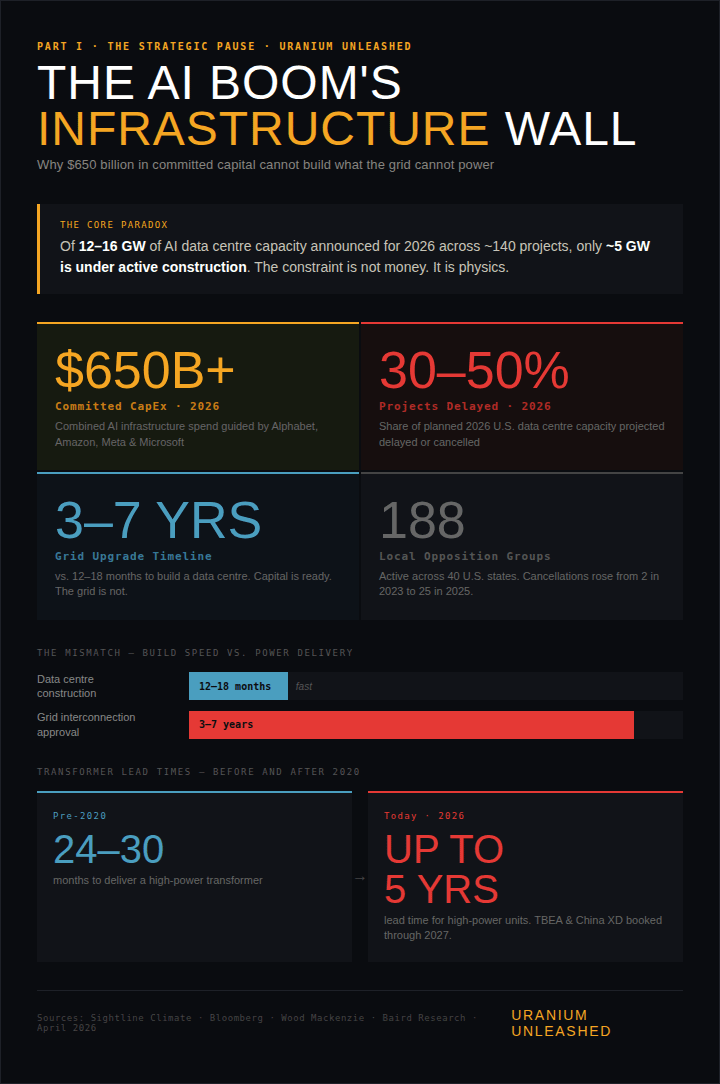

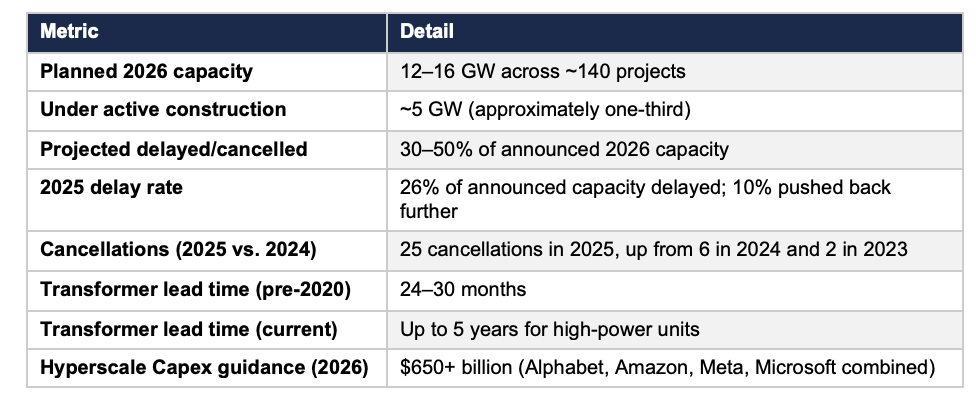

The rapid acceleration of AI data center development in the United States has entered a critical inflection point. What the industry is experiencing is not a collapse in demand, but a structural confrontation with the physical limitations of the American power grid and a deepening scarcity of foundational electrical components. Between 30% and 50% of all AI data centers planned for deployment in 2026 are now projected to be delayed or cancelled outright, according to analysis from Sightline Climate and reporting by Bloomberg. Of approximately 12–16 GW of announced capacity, only around 5 GW is currently under active construction.

For the nuclear energy sector — which had been positioned as the primary catalyst for powering the AI boom — this phase represents a necessary transition from speculative, short-term expectations to a more disciplined, long-term capital deployment strategy. The hyperscalers are not retreating from nuclear; they are recalibrating timelines. The fundamental thesis remains intact: as AI clusters scale toward gigawatt-level requirements, nuclear energy is the only proven technology capable of delivering 24/7, carbon-free baseload power at scale.

The Infrastructure Wall

The Grid Interconnection Gap

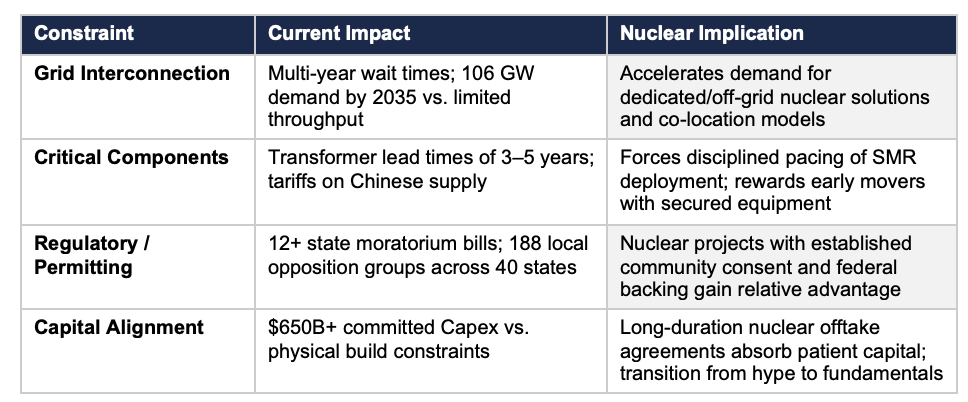

The primary driver of the current slowdown is a severe disconnect between the speed at which digital infrastructure can be deployed and the prolonged timelines required for energy grid upgrades. Data centers can be commissioned and built within 12 to 18 months. However, meaningful upgrades to transmission and distribution networks typically require 3 to 7 years to complete, owing to complex permitting requirements, land acquisition challenges, and intricate technical engineering.

This mismatch has created a situation where capital is ready, land is available, and compute hardware is on order — but the grid simply cannot deliver the power to the site. BloombergNEF projects that U.S. data center power demand will reach 106 GW by 2035, more than double current levels. The challenge is not a shortage of proposed projects; it is getting them physically connected to the grid and operational.

The Electrical Equipment Bottleneck

Compounding the grid interconnection problem is an acute global shortage of essential electrical hardware. Transformers, switchgear, batteries, and advanced electrical management systems form the backbone of any data center’s power delivery infrastructure. Though this equipment represents less than 10% of total project cost, a delay in any single element of the power chain can halt an entire project.

The scale of the shortage is striking. Before 2020, high-power transformer delivery in the U.S. typically took 24 to 30 months. Today, lead times can stretch to five years. China remains the world’s largest producer of the electrical equipment required, yet U.S.–China trade tensions and tariff structures are further constricting supply. Copper, a core transformer component, now faces a 50% tariff under the April 2026 expansion of metals duties. The two dominant Chinese transformer suppliers to the U.S. market, TBEA and China XD Group, report their order books filled through 2027.

Domestic manufacturers are responding, but not fast enough to close the gap within the current planning horizon. Eaton has committed $340 million to a new South Carolina plant targeting 2027. Siemens Energy is building its first U.S. large power transformer plant in Charlotte, North Carolina, also targeting 2027 production. GE Vernova has expanded capacity through its Prolec acquisition. Yet collectively, Wood Mackenzie has cautioned that even with nearly $1.8 billion in announced North American manufacturing expansions, the shortage of critical transformer types is likely to worsen before it improves.

The Bottleneck in Numbers

Companies Pressing Pause

The strategic pause is not limited to smaller operators. Several of the world’s most capitalised technology companies have been forced to scale back, delay, or fundamentally restructure their data center deployment plans.

OpenAI / Stargate

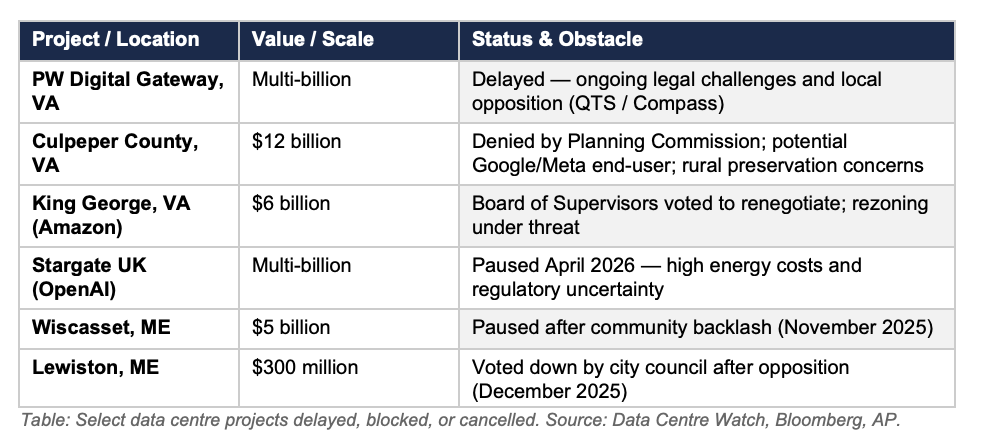

OpenAI’s Stargate programme — announced as a $500 billion, four-year AI infrastructure initiative — has encountered delays across multiple geographies. The domestic U.S. programme, anchored by a 1.2 GW campus in Abilene, Texas, was stalled for months by disagreements between OpenAI, Oracle, and SoftBank over site ownership and system control. Reports indicate that Oracle and OpenAI ended plans to expand the Abilene campus from 1.2 GW to the originally planned 2.0 GW, citing financing difficulties and changing capacity needs.

Internationally, OpenAI paused its multi-billion-pound Stargate UK project in April 2026, citing high energy costs and regulatory uncertainty. The project, announced in September 2025 in partnership with Nvidia and Nscale, had targeted up to 8,000 GPUs in early 2026 with plans to scale to 31,000 GPUs. Days later, OpenAI also pulled back from its Stargate Norway deal with Nscale, with Microsoft stepping in to absorb the capacity at a planned 230 MW facility in Narvik. The retrenchment comes as OpenAI tempers spending expectations ahead of a potential IPO, having raised $122 billion at an $852 billion valuation in March 2026.

Microsoft

Microsoft has cancelled or scaled back an estimated 2 GW of data centre projects, according to analysis by TD Cowen. AWS and Microsoft were both observed pausing discussions over data centre leases, particularly in overseas markets. Wells Fargo analysts noted that hyperscaler’s have become “more discerning with leasing large clusters of power” and are tightening pre-lease windows for capacity slated before end-2026. Microsoft has stated it remains on track for approximately $80 billion in AI data centre spending, but acknowledged it may “strategically pace or adjust” infrastructure in some areas.

Amazon Web Services

AWS paused discussions on some data centre leases, primarily in overseas markets, according to Wells Fargo analysts. In Virginia — the epicentre of U.S. data centre development — Amazon’s $6 billion King George County project remains in limbo after the local Board of Supervisors voted to renegotiate the original performance agreement, with community resistance over infrastructure and resource impacts proving a persistent obstacle.

The Rising Political Headwind

Beyond the corporate boardroom, a wave of political opposition is now materially affecting project timelines. Data centre project cancellations more than quadrupled to 25 in 2025, up from just 6 in 2024 and 2 in 2023, according to Baird research. At least 188 local opposition groups now operate across 40 U.S. states.

At the state level, the policy response has been even more significant. As of early 2026, at least 12 states have filed data centre moratorium bills in their current legislative sessions. These include Georgia, Maryland, Michigan, Minnesota, New Hampshire, New York, Oklahoma, Rhode Island, South Dakota, Vermont, Virginia, and Wisconsin. The bills would variously pause construction, suspend tax incentives, or require comprehensive environmental and utility-rate impact studies before new projects can proceed.

In late April 2026, Maine’s legislature passed what would have been the nation’s first statewide data centre moratorium (LD 307), but Governor Janet Mills vetoed the bill because it lacked a carve-out for a $550 million project in the town of Jay. The near miss signals the direction of political travel. The data centre industry can no longer treat community consent as a formality.

Nuclear Energy: From Quick Fix to Baseload Anchor

The Thesis Recalibrated, Not Abandoned

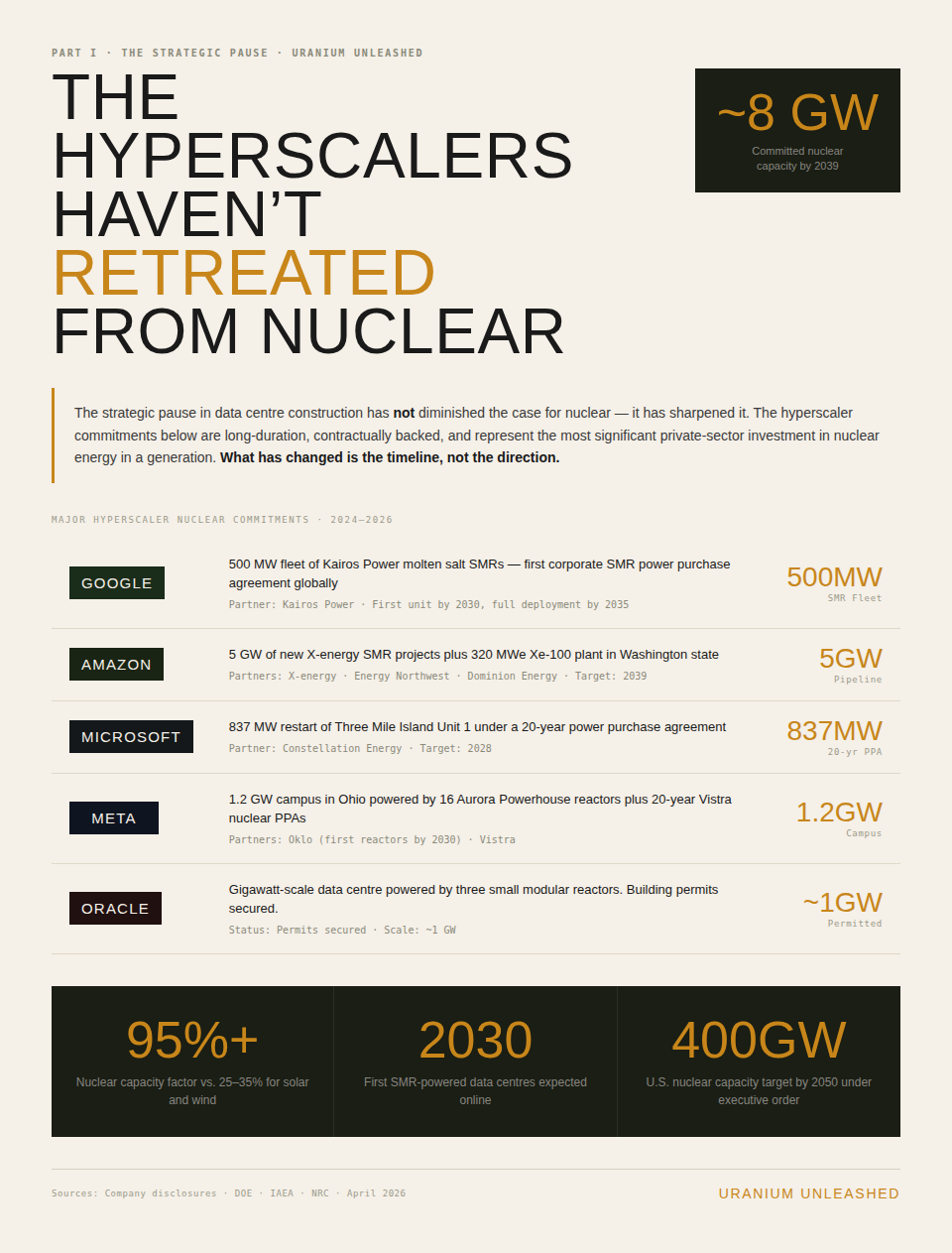

The strategic pause in data center construction has not diminished the case for nuclear energy — it has sharpened it. The infrastructure crisis has reinforced a fundamental reality: as AI clusters scale toward gigawatt-level requirements, intermittent renewable energy sources are insufficient to meet the strict 24/7 reliability standards demanded by high-density computing. Nuclear’s capacity factor exceeds 95%, compared with 25–35% for solar and wind. Its land footprint is minimal. And it is the only proven clean energy technology that can deliver firm, dispatchable baseload power at the scale the AI economy requires.

What has changed is the timeline and the investment posture. The hype cycle — in which nuclear was positioned as an immediate fix for exploding power demand — has given way to a more disciplined framework centred on long-term offtake agreements, strategic site selection, and regulatory pathway de-risking.

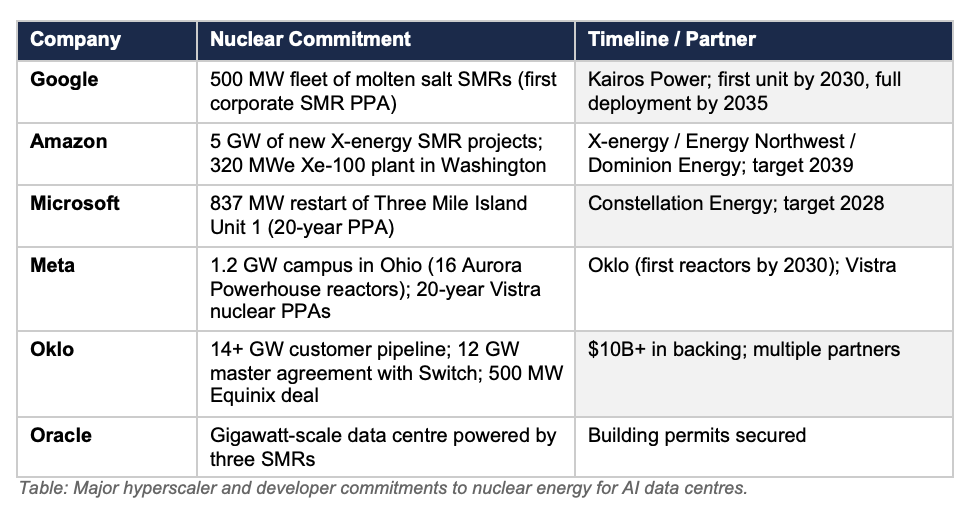

Hyperscaler Nuclear Commitments

The scale of commitments from the world’s largest technology companies to nuclear energy remains substantial and continues to grow.

The SMR Pipeline

Small modular reactors sit at the centre of the nuclear–AI convergence. SMRs produce up to 300 MW of power, require approximately 50 acres of land, and deliver an uninterrupted energy profile that renewables cannot match. Their modularity allows deployment to scale alongside data center campus expansion — a fundamental design advantage over traditional large-scale nuclear plants.

Key developments in the SMR pipeline include TerraPower breaking ground on its Natrium reactor in Kemmerer, Wyoming, in June 2024 — the first commercial advanced reactor construction in the United States. The DOE has selected the Tennessee Valley Authority and Holtec as the first recipients of $400 million each in cost-shared funding to advance early SMR deployments. And in February 2026, Clayco announced plans to oversee delivery of a nuclear-powered AI data center campus at Idaho National Laboratory, featuring a phased approach starting with the data center followed by a 60 MW MK60 SMR.

BloombergNEF expects approximately 15 reactors to come online globally in 2026, adding close to 12 GW of new capacity. China’s Linglong One SMR is scheduled to begin commercial operations in the first half of 2026, which would make it the world’s first commercial onshore SMR. On the policy front, U.S. executive orders have targeted an increase in national nuclear capacity from approximately 100 GW in 2024 to 400 GW by 2050.

The Structural Shift: From Hype to Fundamentals

What the Pause Means for Nuclear Investors

The current environment is fundamentally de-risking the nuclear sector. By removing the unrealistic pressure to deliver immediate power for AI data centres, the strategic pause provides critical breathing room for regulatory bodies to streamline licensing processes, for the supply chain to address equipment constraints, and for developers to advance reactor technologies through proper engineering and safety validation.

For uranium specifically, the demand signal is not weakening — it is extending. The shift from “quick fix” to “baseload anchor” means that new reactor deployments, once operational, will consume uranium fuel for decades. The hyperscaler commitments detailed in this report represent long-duration, contracted demand that the uranium market has not yet fully priced in. Meta’s Oklo partnership alone involves prepayments to secure nuclear fuel, signalling a new class of technology-sector buyer entering the fuel procurement chain.

The Constraint Framework

5. Outlook and Conclusions

The strategic pause in AI data center construction is not a signal that the AI revolution is slowing. It is an acknowledgment that the physical world has constraints that no amount of capital can instantly override. Demand for AI compute continues to grow. What has changed is the industry’s reckoning with the infrastructure required to support it.

For the nuclear sector, three conclusions follow:

• The demand thesis is intact and strengthening. Hyperscaler commitments to nuclear energy are long-duration, multi-billion-dollar, and backed by the world’s most capitalised companies. These are not speculative bets — they are strategic infrastructure decisions.

• Timeline realism is an asset, not a liability. The shift from “nuclear as quick fix” to “nuclear as baseload anchor” aligns the investment case with the actual deployment cadence of advanced reactor technologies. The first SMR-powered data centres are expected online by 2030, with fleet-scale deployment through the mid-2030s.

• Uranium demand is extending, not contracting. Each reactor that comes online represents decades of contracted fuel consumption. The market has not yet fully priced in the structural demand implied by the current pipeline of hyperscaler nuclear commitments, DOE-backed SMR projects, and executive-order-driven capacity targets.

The companies and investors who will benefit most from the AI–nuclear convergence are those who understand that this is a decade-long infrastructure play, not a quarterly earnings story. The pause is not the end of the opportunity — it is the beginning of the disciplined phase.

Sources and References

Bloomberg, U.S. Data Centre Boom Relies on Hard-to-Find Electrical Equipment (April 1, 2026)

Bloomberg, OpenAI Pauses Stargate UK Data Centre Citing Energy Costs (April 9, 2026)

CNBC, OpenAI Pulls Back from Stargate Norway Data Centre Deal (April 15, 2026)

Tom’s Hardware, Half of Planned US Data Centre Builds Delayed or Cancelled (April 2026)

Construction Dive, What’s Stalling Data Centre Projects? Public Opposition and Power Access (April 2026)

Sightline Climate, U.S. Data Centre Capacity Analysis, via Bloomberg and Tech Spot (2026)

Good Jobs First, Data Centre Moratorium Bills Are Spreading in 2026 (March 2026)

AP / U.S. News, Maine Governor Vetoes Data Centre Moratorium (April 24, 2026)

Data Centre Watch, $64 Billion of Data Centre Projects Blocked or Delayed (2025–2026)

Power Magazine, Transformers in 2026: Shortage, Scramble, or Self-Inflicted Crisis? (January 2026)

Latitude Media, Why AI Data Centres and Offshore Wind Face the Same Delays (February 2026)

IAEA, Data Centres, AI and Cryptocurrencies Eye Advanced Nuclear

iRecruit, SMR Data Centres: Nuclear Power & AI (March 2026)

Carbon Credits, 2026: The Year Nuclear Power Reclaims Relevance (December 2025)

TD Cowen, Microsoft Data Centre Cancellations Analysis (2025–2026)

IT Pro, Tech Giants Hitting the Brakes on Data Centre Plans (2025)

Disclaimer

This report is published by Uranium Unleashed for informational and analytical purposes only. It does not constitute investment advice, a solicitation to buy or sell securities, or a recommendation of any specific investment strategy. The author may hold positions in securities discussed. All information is believed to be accurate as of publication but is provided without warranty. Readers should