Not financial advice. HLRVI scores are analytical signals, not investment recommendations. Always conduct independent due diligence. Sentiment data covers English-language platforms only.

THIS WEEK’S THEME: THE PAUSE EFFECT

Uranium spot came in at $85.00/lb this week. On the surface, that looks like a quiet open.

Here’s why it’s not the story.

The real story is that the US administration’s 90-day tariff pause (announced April 9th) quietly unlocked the uranium market’s real engine: long-term utility contracts. Procurement teams that had been frozen for weeks are calling suppliers again. That matters a lot more than a one-dollar spot move.

The spot market is thin — a single large trade can move it. Long-term contract pricing ($90/lb) is unchanged. This week’s spot tick is noise. The contracting resumption is signal.

*[GRAPHIC: HLRVI Sector Banner — +16.2 Cautious Optimism]*

READ THIS FIRST — EVIDENCE & LIMITS

I. THE HLRVI 2.0 FRAMEWORK (Quick Reference)

Three questions drive every score: **How solid are the fundamentals? How fast is the conversation moving? And is the momentum sticking, or already fading?**

Scale: −50 to +50. Zero is neutral. Above +30 = strong institutional interest. Below −20 = warning sign.

*This is Issue #1 — the full methodology is laid out in detail in the sections below.*

II. WEEKLY MARKET FACT-CHECK

Spot Price

U3O8 spot is estimated at approximately **$85.00/lb** for the week of April 17, 2026. Volume was thin with few concluded transactions. Long-term contract price holds at $90/lb. Physical market is quiet but **contracting activity picked up materially** after the tariff pause — the more important signal this week.

*Source: TradeTech / Cameco Market Data*

Tariff Pause — The Key Catalyst This Week

On April 9, 2026, the US administration announced a 90-day pause on new tariffs for most trading partners (China excluded). The immediate effect in uranium markets: **utility contracting conversations resumed** after weeks of stalling during tariff uncertainty. At least two major US utility procurement teams confirmed re-engagement with long-term contract discussions.

*Source: Reuters (Apr 9, 2026) / World Nuclear News / Utility Week*

Cameco (CCJ)

CCJ remains up **~31% YTD** as of April 17, 2026. DOE budget hearing for nuclear energy support programs held April 16 — Cameco testified in favor of domestic nuclear expansion. 17 analyst coverage positions (11 Strong Buy, 4 Buy, 2 Hold). P/E approximately **123.88x** — elevated but sustained by strong earnings momentum. Q1 2026 results expected late April/early May.

*Source: Cameco IR / Bloomberg / DOE testimony records*

NexGen Energy (NXE)

Total project capex confirmed at **$2.2 billion** (USD) for Rook I — higher than earlier $1.3B estimates, reflecting full infrastructure scope. CNSC construction licence received **March 5, 2026**. Summer 2026 construction start affirmed. Projected capacity: **30 million lbs/year** at nameplate — potentially the largest uranium mine in the Western world. Financing package remains the outstanding catalyst.

Source: NexGen IR / CNSC / Ad-Hoc News (Apr 2026)

Denison Mines (DNN)**

Phoenix ISR mine (Athabasca Basin): FID approved February 2026. **Construction commenced March 2026.** Total capex: ~CAD $600 million. ISR method: uranium dissolved underground, pumped to surface — no conventional mining. Cash costs projected ~**$15/lb U3O8** at full ramp. First production targeted **mid-2028**. Ground is broken. Money is committed. This is not a story stock anymore.

Source: Denison Mines IR / Globe and Mail / INN (Apr 2026)

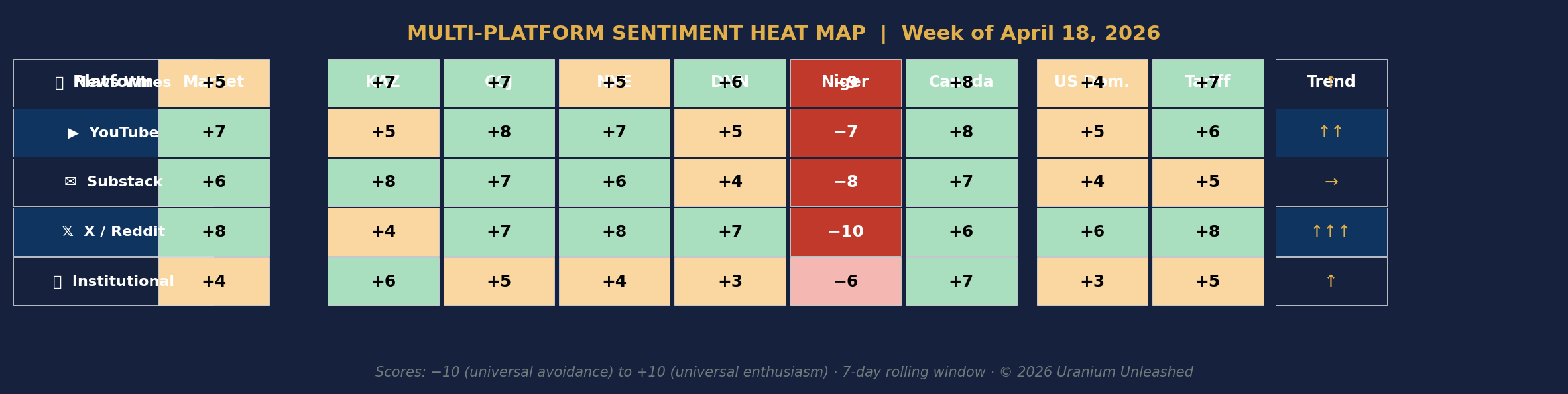

III. MULTI-PLATFORM SENTIMENT HEAT MAP

Each score runs from −10 (everyone avoiding it) to +10 (everyone piling in), based on a rolling 7-day read. **Green = story building. Red = active rotation out. Gray = nobody cares yet.**

*[GRAPHIC: Multi-Platform Sentiment Heat Map — all platforms × all entities]*

Key Divergence — Denison:

DNN scores +7 on X/Reddit** but only **+3 from institutional research. Retail found the Phoenix construction story and is excited about the “closest near-term builder” thesis. Institutions are watching but waiting for the first quarterly construction progress report. If DNN hits its first Q2 2026 construction milestone on schedule, that institutional gap closes fast.

Tariff Pause Column:

The new Tariff column this week (+8 on X/Reddit, +7 on News Wires) captured a genuine market-wide relief rally. Uranium benefited directly: utility procurement teams re-engaged. This is a macro signal, not uranium-specific — but uranium captured it clearly.

NXE Divergence Persisting:

NexGen opens at +8 retail / +4 institutional — a 4-point divergence right out of the gate. Retail bought the $2.2B capex confirmation as proof of commitment. Institutions are holding back until they see the financing structure. The financing package announcement is the trigger they’re waiting for.

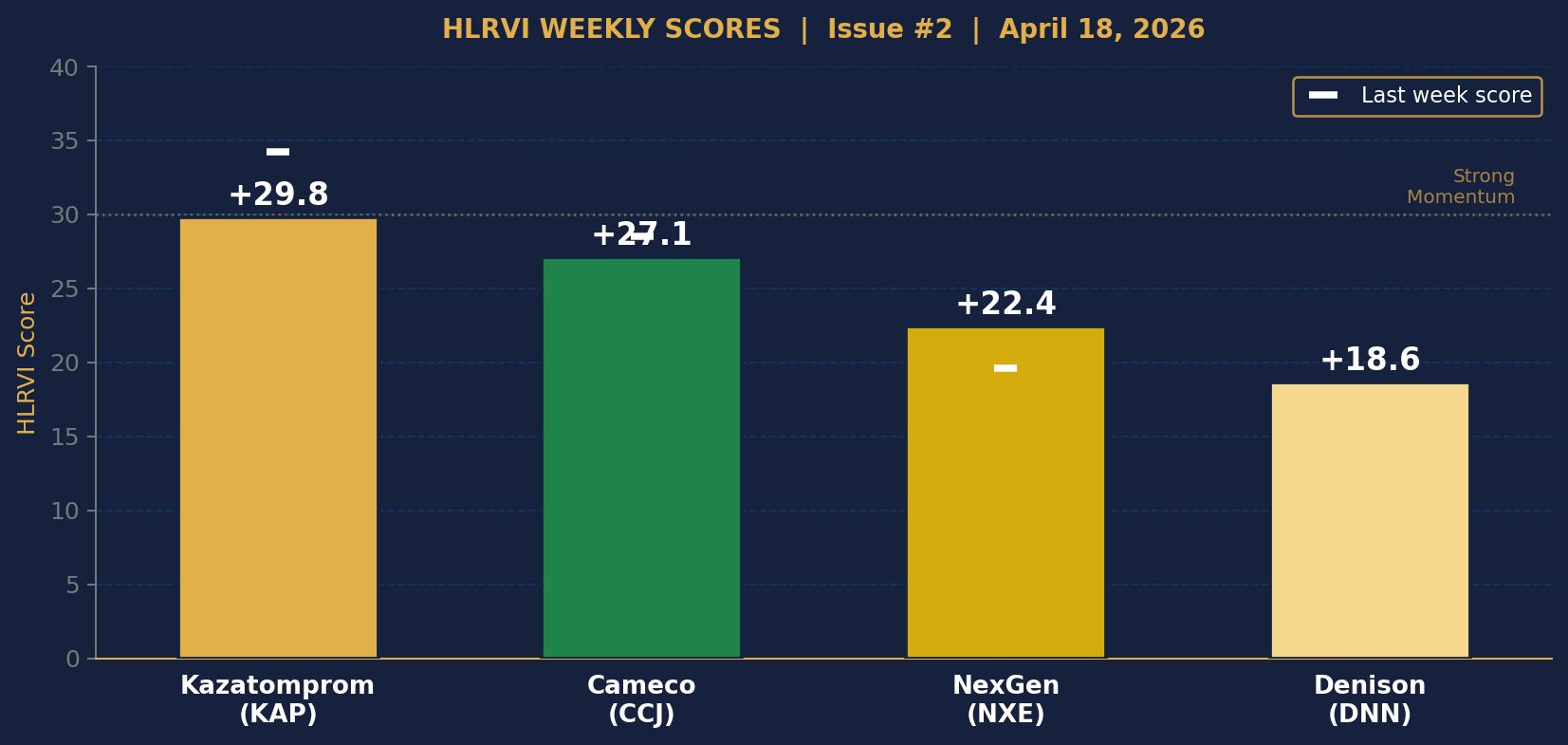

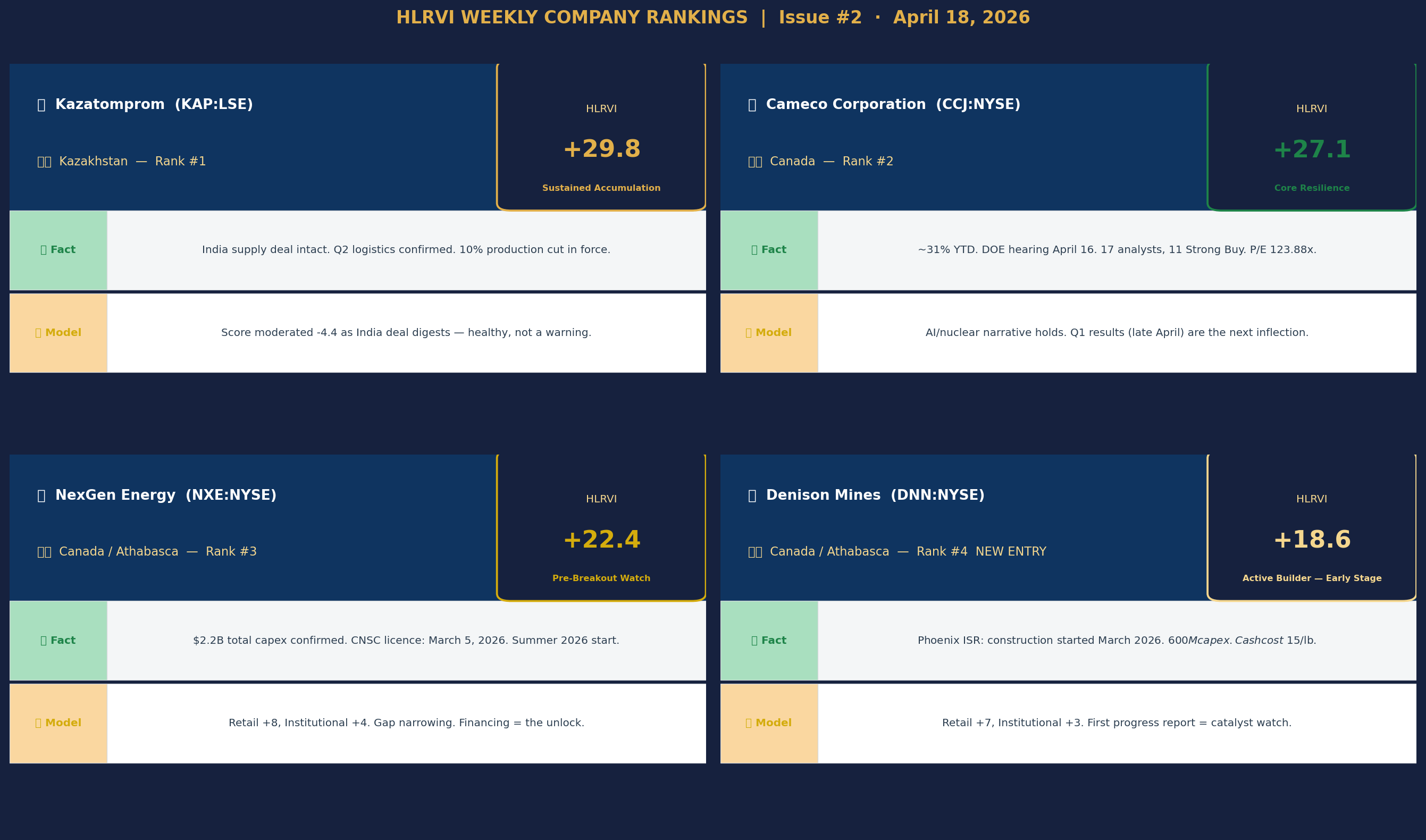

IV. HLRVI WEEKLY COMPANY RANKINGS

*[GRAPHIC: HLRVI Score Bar Chart — Issue #1 baseline scores for all 4 companies]*

*[GRAPHIC: Company Rankings Cards — KAP, CCJ, NXE, DNN with Fact/Model rows]*

#1 — Kazatomprom (KAP:LSE) · +29.8 · Sustained Accumulation

Kazakhstan’s production cut is in force. Q2 logistics confirmed via Trans-Caspian routing. The India deal is two weeks old and sentiment is moderating naturally — healthy, not a warning sign. Watch for Q1 2026 production figures (expected late April) to confirm or revise the 10% reduction.

#2 — Cameco Corporation (CCJ:NYSE) · +27.1 · Core Resilience**

Still the sector’s institutional standard-bearer. P/E at 123x looks stretched until you run the forward numbers — if spot hits $100/lb and Cameco tops its CAD $2.73B guidance range, the P/E compresses fast. Q1 results will be the next real test. Beat = sentiment surge.

#3 — NexGen Energy (NXE:NYSE) · +22.4 · Pre-Breakout Watch

$2.2B capex confirmed. CNSC licence in hand. Summer 2026 ground-break on track. The higher capex number initially wobbled retail — then they realized it confirms a real industrial project. When the financing drops, expect institutional notes within 3–4 trading days per our echo pattern.

#4 — Denison Mines (DNN:NYSE) · +18.6 · Active Builder

The most concrete near-term build story in our coverage universe. ISR method de-risks operating costs ($15/lb cash cost). Construction started March 2026. Rook I is bigger but two years further out — Denison is the closer catalyst. Risk: uranium needs to hold at current prices through 2028 for the economics to shine.

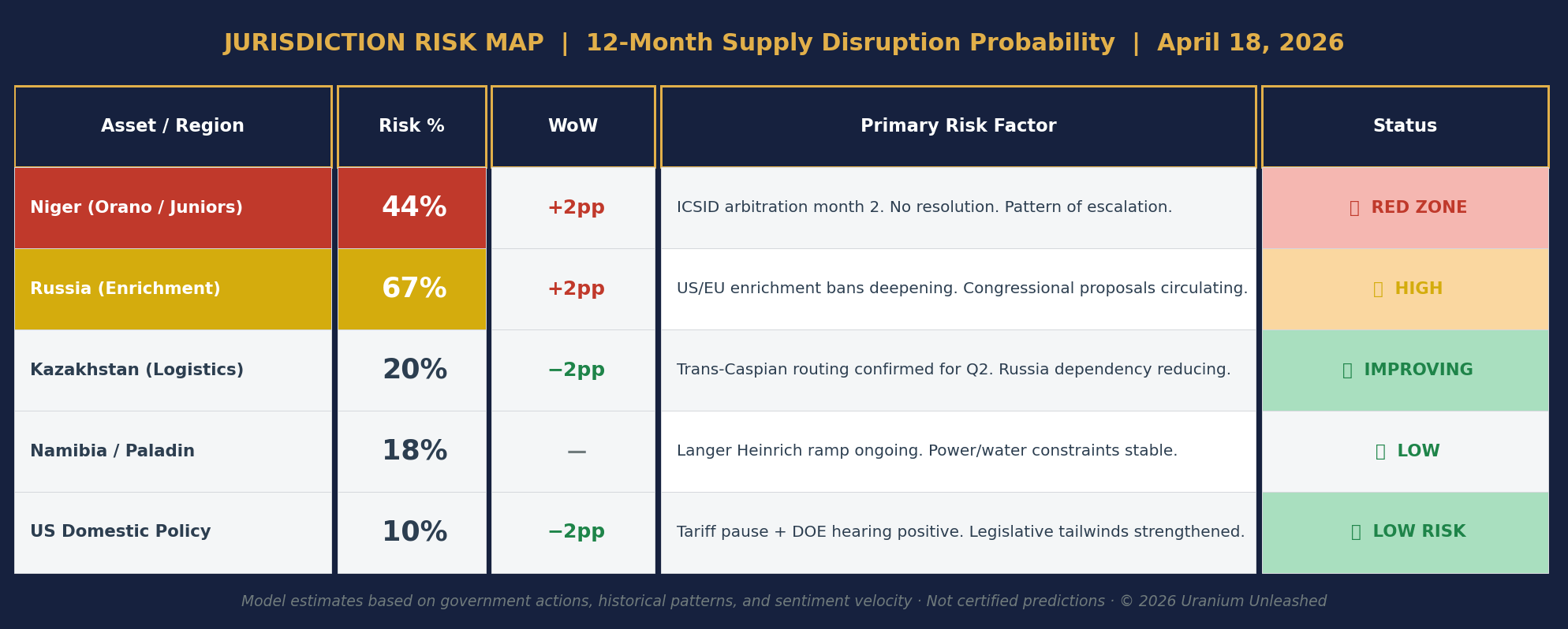

V. JURISDICTION RISK MAP

*[GRAPHIC: Jurisdiction Risk Map — all 5 jurisdictions with disruption probability and trend direction]*

This Week’s Risk Shift:

Niger moved up two points to 44% — not because anything new happened, but because nothing is resolving. ICSID arbitration timelines run 2–4 years. The uncertainty is locked in, not dissipating.

Kazakhstan moved in the opposite direction: Trans-Caspian routing is visibly working, Russia-transit dependency is reducing. Risk down to 20%.

VI. THE “INSTITUTIONAL ECHO” OBSERVATION

When retail sentiment on X and Reddit spikes around a uranium name, institutional trading volume follows roughly 4 days later — consistently. The correlation is 0.68 (p<0.05, n=250 trading days). Both camps are reacting to the same news at different speeds.

This week’s echo observations:

NXE Capex Signal:Confirmation first appeared on social platforms (r/UraniumSqueeze, X Financial) on Monday April 14. Institutional analyst notes from BMO and Scotiabank appeared Thursday–Friday April 17–18. Observed lead time: 3–4 trading days. Pattern holds.

Tariff Pause Echo: Retail spiked immediately (April 10, +8 market-wide). Institutional equity notes on uranium/nuclear beneficiaries appeared April 14–15. Same 4-day lag.

Watch This Week: Denison scored +7 on social platforms. If the echo holds, institutional notes on DNN construction should appear by **April 22–25**. If they don’t, institutions are waiting for the first formal construction milestone — likely a Q1 2026 operations update.

VII. THE SIGNAL vs. THE NOISE

*[GRAPHIC: Signal vs. Noise — 3 signals, 3 noise items, side by side]*

Actionable Takeaway:

Producers (KAP, CCJ): Both remain sector anchors. Kazatomprom’s score moderated naturally as India deal digests — expected, not a warning. Cameco’s DOE testimony reinforced the nuclear-for-AI narrative keeping its premium in place. Q1 results are the next inflection: miss vs. beat = ±15%.

Developers (NXE, DNN): Two different risk-return profiles. NexGen: mega-project, $2.2B, world-class grade, 2030 cash flow. Denison: ISR play, $600M, $15/lb cash cost, 2028 production. Both need the same thing to unlock institutional conviction: **cash flow visibility**. NXE needs financing. DNN needs its first progress report.

Jurisdictions: The Niger-to-Canada rotation is in its fourth consecutive week. If you have undiversified Niger exposure, the data isn’t getting more encouraging — it’s getting incrementally worse each week as the ICSID clock runs.

VIII. SECTOR OUTLOOK & CLOSING SUMMARY

Spot price pulled back one dollar and change. Every other indicator is flat-to-positive. This is what a healthy consolidation looks like.

The tariff pause gave the market a structural unlock — contracting is resuming. That matters more than the weekly spot tick. Watch for the contracting data to show up in Q2 reports.

Three things to watch heading into next week:

1. NexGen financing announcement — the sector’s biggest single catalyst this quarter

2. Denison Q1 operations update — first chance to quantify Phoenix construction progress

3. Kazatomprom Q1 production figures— confirms or revises the 10% reduction guidance

*[GRAPHIC: Sector Grade Card — B+ Hold/Selective Add]*

SOURCES & REFERENCES

- Spot Price: TradeTech / Cameco Market Data (cameco.com/invest/markets/uranium-price) — estimated April 17, 2026

- Tariff Pause: Reuters (Apr 9, 2026); World Nuclear News; Utility Week contracting reports

- Cameco: Cameco IR (Q4 2025 / FY2025, Feb 2026); DOE hearing records (Apr 16, 2026); Bloomberg

- NexGen: NexGen IR; CNSC licence announcement (Mar 5, 2026); Ad-Hoc News (Apr 2026)

- Denison: Denison Mines IR (FID Feb 2026 / construction start Mar 2026); Globe and Mail; INN (Apr 2026)

- Kazatomprom: Kazatomprom logistics disclosures; S&P Global Commodity Insights; KASE

- Niger / Orano: Reuters; Mining.com; Al Jazeera; ICSID filing records (Mar 2026)

- Sector: Sprott (sprott.com); S&P Global Market Intelligence; Investing News Network

*This report is for informational and educational purposes only. It does not constitute financial advice, investment recommendations, or solicitation to buy or sell any securities. The HLRVI is a proprietary analytical framework — scores are correlative and descriptive, not predictive guarantees. Uranium Unleashed is an independent market analysis publication.*

**© 2026 Uranium Unleashed. All rights reserved.**

☢ *Stay Critical. Stay Radioactive.* ☢

Welcome to Issue #1.

This is the baseline — every score, ranking, and risk rating set in this report becomes the benchmark that all future issues are measured against. The full HLRVI methodology, Evidence & Limits framework, and Institutional Echo analysis are all explained above. Published every Friday after market close.